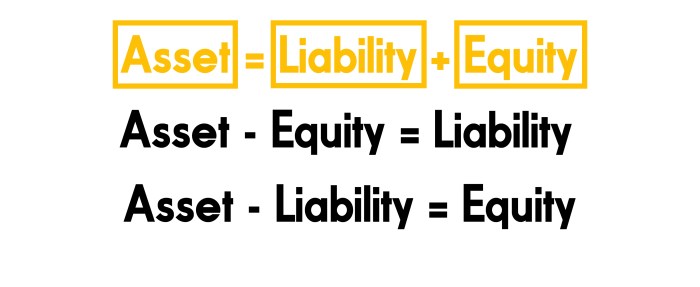

All of the Entries in the preceding Sections of the SMP Compendium have been building toward the basic articulations of a distinct accounting system for the Work-Standard. Since the Work-Standard relies on Arbeit and Geld as its definitions of wealth in the Socialist Nation, the “Double-Entry Account Bookkeeping” employed under Neoliberalism will be no longer be tolerated. The Explicit Intent here is that Double-Entry Account Bookkeeping was designed to be used in the accounting of Kapital and Schuld. Never was it designed for the Accounting Profession to account for the Quality of Arbeit and the Quality of Geld. This fact alone is discernible from its basic fundamental equations for Quantity of Kapital and Quantity of Schuld:

The “Asset” refers to the sum of the Quantity of Schuld as “Liability” and Quantity of Kapital as “Equity.” With “Equity” as Quantity of Kapital, an Accountant can immediately uncover someone’s Net Worth, as demonstrated by the following operation:

When the Accountant needs to know the precise of details behind the Quantity of Kapital for most privatized commercial firms, the fundamental equation of Double-Entry Account Bookkeeping can be expanded further as:

The “Liability” is now identified as the Quantity of Schuld that accrues as a result of trying to create more Kapital. The “Equity” becomes the difference between the sum of existing Kapital and how much Kapital was earned from transactional sales and all expenditures associated with operating a privatized commercial firm and any Kapital spent on personal Incentives. The specifications for how Double-Entry Account Bookkeeping function and its historical background deserve their own Treatise. For now, the purpose of this Entry is to introduce the Work-Standard’s proposed alternative to Double-Entry Bookkeeping.

All Socialist, Corporatist, Syndicalist and State Capitalist VCS Economies, Reciprocal-Reserve Banking Systems, and States rely on “Command-Obedience Account Bookkeeping.” Command-Obedience Account Bookkeeping is an application of the Intents of Command and Obedience, allowing Accountants, Economic Planners and Inspectors to determine how much Arbeit and Geld is being generated by individual Vocations, Professions, Enterprises, Industries, and Economic Sectors. It is designed to be reapplied to the State’s Ministries, Departments and Offices as well as the Student Government’s Student Economy, and the National Intranet’s Digital Economy. Instead of a simple arithmetic equation with variables of “Asset,” “Liability” and “Equity,” Command-Obedience Account Bookkeeping employs a different trio of variables:

In financial ledgers, reports and statements under Command-Obedience Account Bookkeeping, the “State” is always listed on the left-hand side as the “Obedience-side” and the “Totality” and “Self” as the “Command-side.” Here, the “State” is the combined sums of Arbeit and Geld generated by the “Totality” and the “Self.” The finances of the State are the finances of the Totality and the Self. It represents the national income of the entire country, denominated in its own Sociable Currency. Both Totality and Self are equally capable of creating Arbeit and Geld.

All three of those basic equations are needed by an Accountant to know the “Total Productive Potential (TPP) Account” of the Socialist Nation. The TPP Account is one of the three accounts employed by the Work-Standard as part of its own Chart of Accounts (CoA) and its own System of National Accounts (SNA). I just established the Work-Standard’s version of the CoA, and the Central Bank will need its distinct SNA, which requires the TPP Account and two other main accounts to acquire the final TPP value. Remember all units of Sociable Currency in circulation, as the “Requisitionary Productive Forces (RPF),” must be on par with TPP, otherwise the Socialist Nation will begin accumulating Sovereign Schuld as a consequence. The equation for the Life-Energy Reserve’s Final TPP Value and the equation for the TPP Account are as follows:

To find the Life-Energy Reserve’s Final TPP Value requires finding the sum of the TPP Account, the “Life-Energization Reciprocity (LER) Account,” and the “State Investment-Economic Foreignization (SI-EF) Account.” In order to uncover the TPP, LER, and SI-EF Accounts, an Accountant and their Economic Planner will need to familiarize themselves with the Work-Standard’s SNA, the “Worksheet of Sociable Accounts (WSA).” Below is a completed copy of the WSA containing all of the variables to find the Life-Energy Reserve’s TPP value:

But in any serious application of the Work-Standard, no Economic Planner and their retinue of Accountants are going to know every detail of the VCS Economy nor should they have to if they are only assigned to an individual Enterprise. In fact, it is inevitable for them to have a partially incomplete WSA; the only ones that would have a complete WSA are the Head of State, Head of Government, State Council, Central Bank, the Central Planners at the Ministry of Economics, and the Superintendents at the Ministry of Finance. The Council State can compile the information for its own National Accounts, State Accounts, Domestic Accounts and Foreign Accounts, but it will need information from the Economic Planners and Accountants to complete the rest of the WSA in order to uncover the Final TPP Value.

What the Economic Planners and Accountants of every Enterprise must have filled out on their own WSAs are their Enterprise’s National Accounts, Communion Accounts, Social Accounts, and Household Accounts. Thus, when an Economic Planner needs to know the contributions of Arbeit and Geld for their own Enterprise, they would request their Accountants to provide them with three financial reports: the “WSA Workflow Statement,” “WSA Income Statement,” and “WSA Balance Sheet.”

For the purposes of the SMP Compendium, I will demonstrate how to complete the WSA and all three of those financial reports over the court of the Section. In the next Entries, we will be focusing on how to find the Quality of Arbeit (QW) and Quality of Geld (QM). We need those two if they are going to determine the value of the LER Account as the sum of the “Real Total Economic Potential (RTEP)” and the “Real Total Financial Potential (RTFP)” respectively.

Categories: Compendium

Leave a comment