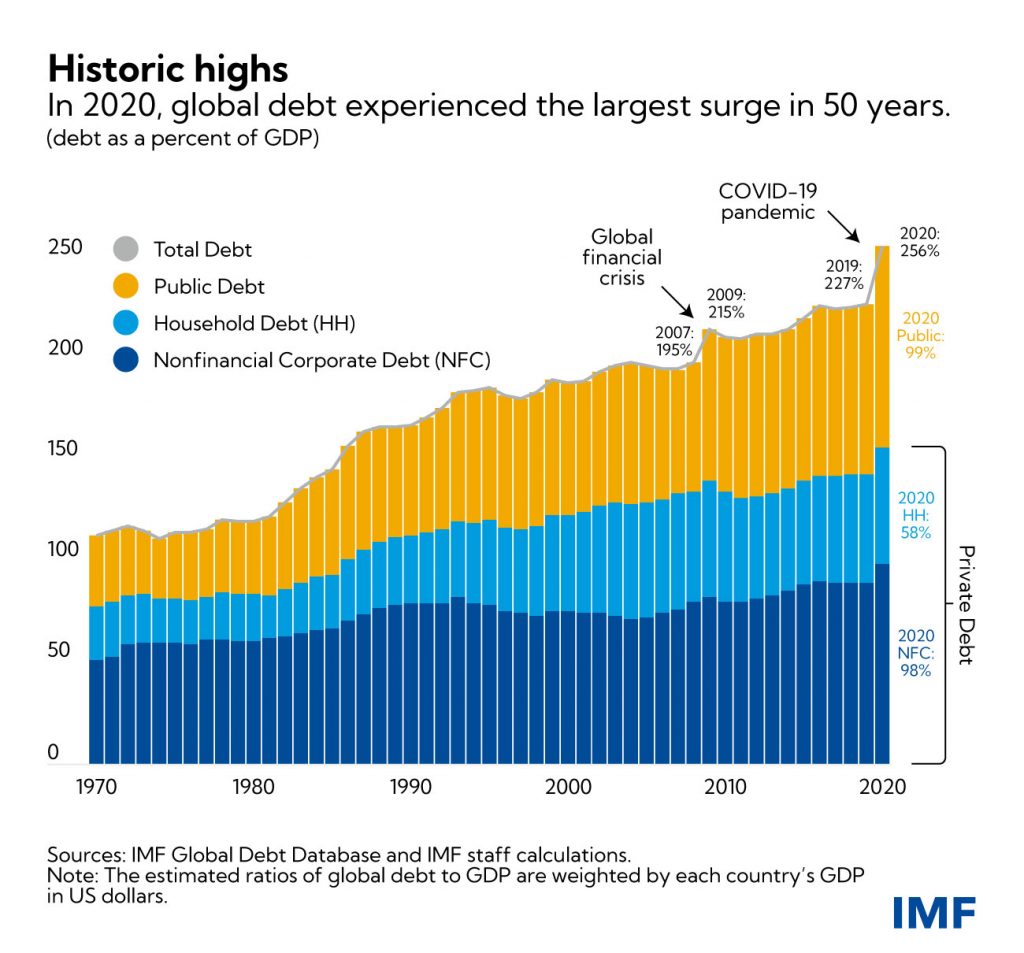

“The large increase in debt was justified by the need to protect people’s lives, preserve jobs, and avoid a wave of bankruptcies. If governments had not taken action, the social and economic consequences would have been devastating.

But the debt surge amplifies vulnerabilities, especially as financing conditions tighten. High debt levels constrain, in most cases, the ability of governments to support the recovery and the capacity of the private sector to invest in the medium term.

A crucial challenge is to strike the right mix of fiscal and monetary policies in an environment of high debt and rising inflation. Fiscal and monetary policies fortunately complemented each other during the worst of the pandemic. Central bank actions, especially in advanced economies, pushed interest rates down to their limit and made it easier for governments to borrow.

Monetary policy is now appropriately shifting focus to rising inflation and inflation expectations. While an increase in inflation, and nominal GDP, helps reduce debt ratios in some cases, this is unlikely to sustain a significant decline in debt. As central banks raise interest rates to prevent persistently high inflation, borrowing costs rise. In many emerging markets, policy rates have already increased and further rises are expected. Central banks are also planning to reduce their large purchases of government debt and other assets in advanced economies—but how this reduction is carried out will have implications for the economic recovery and fiscal policy.

As interest rates rise, fiscal policy will need to adjust, especially in countries with higher debt vulnerabilities. As history shows, fiscal support will become less effective when interest rates respond—that is, higher spending (or lower taxes) will have less impact on economic activity and employment and could fuel inflation pressures. Debt sustainability concerns are likely to intensify.”

With 2021 coming to a close, I now would like to inform everyone about my plans going forward for the next two years. There are currently four ongoing plans regarding The Fourth Estate. There will still be more of the usual Thus Spoke Lenin and Economic History Case Studies Posts. However, I will be focusing more the completion of the three Treatises that I currently have available on my Blog.

I have alluded to this concept of Financial Warfare repeatedly throughout various Posts, in The Work-Standard and The Third Place. In the context of Military Science, nation-states have yet to give it actual form due to the limited capabilities of Kapital and Schuld. With the Work-Standard, the ongoing Revolution in Financial Affairs (RFA) has gotten a lot more exciting because the whole world, not just America, is literally drowning in a deluge of Kapital and Schuld. Currently, I have a multitude of scenarios and grand strategies being concocted at the moment in order to assess the strategic, operational and tactical capabilities of the Work-Standard. This Treatise focuses on the UFSE and its School of Financial Warfare, pitting the “Neumann Knights” against an OPFOR (Opposing Force) to be referred to therein as the “Newman Vikings.” My goal is to assess the worldwide implications of the Work-Standard from variety of vantage points and perspectives. There is no doubt in my mind that the military-industrial capabilities of the Work-Standard are discernible within its own metaphysics.

Like any form of scenario planning, I will include Financial Warfare with an overarching story and background derived from what was already discussed in the previous two Treatises. The Aesthetics of Heroic Realism are applicable here. We will have the American SSE be split into two halves operating on the East and West Coasts. Two styles of governance, two opposing Federalisms, one Eternal Divergence emanating from the American Essence itself.

Categories: Financial Warfare

{kind=link}

{kind=link}

Leave a comment