“Stagflation seems to be a word that we’ve been hearing a lot of recently. With the CPI report showing that inflation had slowed less than expected, stagflation concerns became even louder. However, for the average person, the term probably has never been defined. So, what is stagflation? Today we’ll look at what stagflation is, as well as how it impacts you and the broader economy.”

-Gabriel Shabat, “What is Stagflation,” May 16, 2022

Another trend which emerged in the wake of the Coronavirus Pandemic is the potential reoccurrence of Stagflation. Comparisons to the 1970s have been made in some discussions of the concurring trends of rising Inflation and constant Unemployment Rates. The question remains is whether or not these trends should be interpreted as signs of a second occurrence of Stagflation. While some Liberal Capitalists are entertaining fears that this is definitely the case, not everyone appears to be convinced. It would seem that there is a discrepancy among others who insist on the need to define what constitutes as Stagflation and whether such characteristics apply to present economic conditions in Western countries.

As a primer for the crux of this discussion, an article appeared in The New York Times about Ben Bernanke of Great Recession infamy and his warnings of Stagflation. The article was reporting on statements made by Bernanke in a recent interview where he said that the Federal Reserve’s current monetary policies has proven to be a “mistake.” It was a “mistake” insofar as not enough was being done and what is being done has been a case of ‘too little, too late’. With this conclusion in mind, Bernanke insisted that there is going to be a repeat of Stagflation, predicting that it might occur within the next “year or two.”

Similarly, I found an academic journal article from Markus Demary and Michael Hüther in the German economic policy journal, Intereconomics. The following is a passage where they discuss about the implications of Stagflation and its likelihood in Europe. I have emphasized the most relevant sections for the sake of reference:

“The voices warning of sustained inflation are becoming louder in the face of unusually high price increases. There is concern about changing inflation expectations. Added to this are worries about a weak economic phase, which brought the term stagflation back into the media after decades. On 26 October 2021, the Frankfurter Allgemeine Zeitung pronounced ‘Germany is facing stagflation’. Roubini (2021) stated early last year: ‘Inflation is rising in the United States and many advanced economies, and growth is slowing sharply, despite massive monetary, credit and fiscal stimulus’. Stagflation is not a short-term phenomenon but rather reflects a prolonged stagnation in growth with equally persistent inflationary pressures. In the 1970s, the decade of stagflation, this resulted from a run-up to higher inflation rates, the surprise inflation caused by the oil shortage in 1973 and excessive demands on companies in the accelerated structural change under the banner of automation.

There are some factors that differentiate the situation in the past from the situation today. The wage and financial policies in the 1970s were too expansionary given the economic situation. The central banks had to build a reputation for themselves in the fight against inflation while getting accustomed to the monetary system that emerged after the collapse of Bretton Woods. The insight that a drop in prices would not solve any problems, but rather postpone them, only prevailed later. The era of accelerated globalisation and the liberalisation of international capital movements began after 1980. This was accompanied by new growth opportunities: Cost advantages and market integration in competitive markets resulted in continued price advantages for consumers.

Current stagflation risks must take permanent inflation effects into account while also analysing the growth prospects in the medium term. Decarbonisation affects both contexts because, in addition to the effects of the CO2 price, it can lead to excessive demands on companies in structural change. In addition, there is the digital transformation, which is a disruptive threat to business models, and which is further increasing the pace of structural change. Ultimately, the recently strengthened protectionism and the global system conflict mean that the global division of labour does not result in any relief in price developments or in growth per se.”

In essence, Demary and Hüther maintained that while the likelihood of Stagflation is still unlikely, the possibility of its reoccurrence will not be an exact duplicate of what occurred in the 1970s. The extent of Globalization, particularly the movements of Kapital and Information across international borders, was nowhere as pervasive back then as it is today. There was no Pandemic, Climate Change had yet to be seen as a major environmental issue, and the central banks of the Western countries were still adjusting to the Death of Bretton Woods. If Stagflation were to occur today, it will have to be the product of the flux of contemporary events. Looming against the backdrop of everything is the question of whether the Inflation Rates of the Western nations are permanent or temporary. Even now, it remains to be seen if the Inflation Rates sustained during the Coronavirus Pandemic is permanent or temporary.

What compelled people to argue that Stagflation is going to happen or is happening? The answer lies in the definition of what is defined as Stagflation in mainstream neoclassical economics. The conventional definition of Stagflation is that it is the consequence of stagnant Kapital Accumulation coupled with high Inflation and Unemployment Rates. The amount of Kapital being generated is being negated by Currency Depreciation and stagnation caused by the shuttering of economic activities. Expansions of the money supply and subpar implementations of fiscal and monetary policies, in addition to external factors like wars and instable petroleum prices, can amplify its effects. At least, that was the historical case when Stagflation initially happened during the 1970s. The Death of Bretton Woods, the Yom Kippur War, the rise of OPEC, Ayatollah’s Iran and other significant events of the period were all historical events which neoclassical economics has cited as important factors which led to Stagflation.

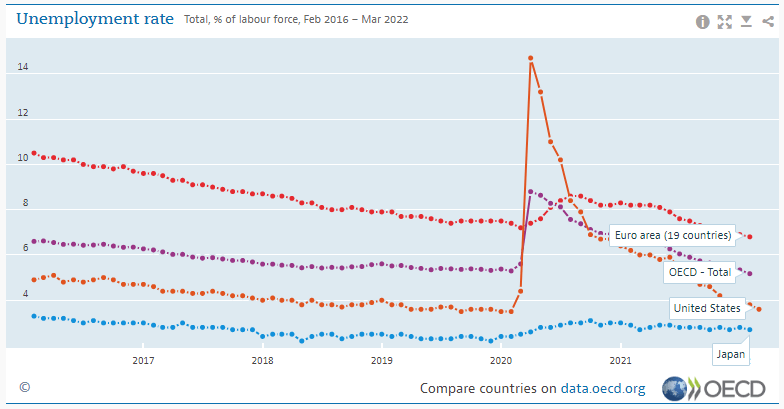

The problem with the describing the current rates of Inflation is that, while Kapital Accumulation is in fact stagnant, the official Unemployment Rate in the US since last April is 3.6%. For comparison purposes, the Unemployment Rates for the EU/NATO countries is 6.90% and 2.70% for post-1945 Japan. The line graph below comes from the OECD, depicting the Unemployment Rate figures from April 2022 to January 2016.

That line graph also came with a bar graph showing the changes in Unemployment Rates among the various individual member-states of the OECD. Notice how most of the member-states that saw the largest increases in Unemployment Rates, denoted in negative values, were also member-states of the EU/NATO.

Given what has already been established about Inflation and Interest Rates in various Western countries, I find the Stagflation comparison to be limited. Granted, I do realize that this might change as time passes, but I have yet to find convincing evidence for Stagflation to be applicable to all Western countries. What I can say is that the ongoing contractionary policy pursued by the Federal Reserve is causing Currency Appreciation for the US Dollar. The rate of Currency Appreciation as of late has proven to be more than enough for the price of Gold to decrease. As the following article from Richard Snow states:

“Gold continued last week’s downtrend and trades lower in the London AM session on Monday. From a fundamental perspective, gold’s outlook is bearish as global interest rates are on the rise in response to surging inflation, worsening the appeal of holding the non-interest-yielding commodity.

The US dollar index (DXY) is a weighted currency index which is generally used as a benchmark for US dollar performance. DXY continues its upward trend after last week’s US inflation data for April – which printed lower than the March print – surprised to the upside. Higher inflation data underpins the value of the greenback at a time when the Fed is fully motivated to raise the Fed funds rate. Current market expectations see the Fed hiking rates a further 190 basis points before the end of the year.

The dollar effect on gold appears to be outweighing the effect of inflation on gold prices. Gold has been lauded as an inflation hedge, however, the relationship holds up better over the long-term, meaning that higher inflation in the short term is actually more likely to result in lower gold prices due to the stronger dollar and higher interest rates adjustment that typically follows.”

These next two graphs are depictions of the US Dollar Index (DXY). The DXY gauges the performance of the US Dollar insofar as it currently represents a form of Kapital. The first graph details the valuations of the US Dollar from the Nixon Shock of 1971 to April 2022. This graph is meant to be compared with the graph, which is the DXY from May 3 to May 16. Even though it was apparently taken around 7:00AM, the fact that the US Dollar relies on Floating Exchange Rates should be accounted for at all times.

Categories: Economic History

Leave a comment