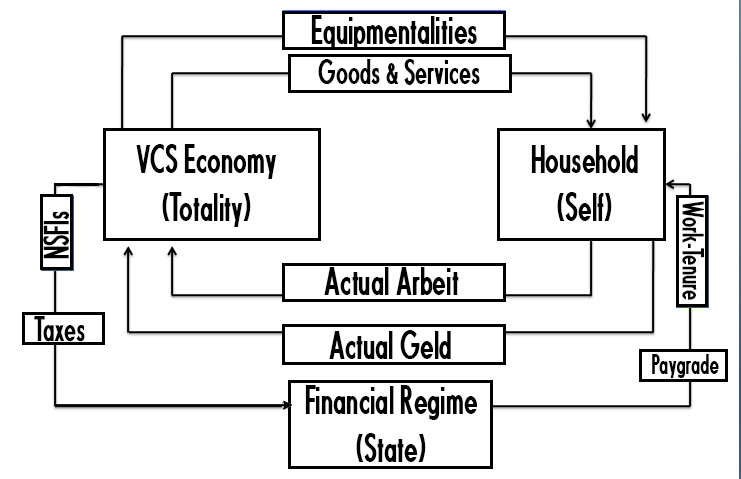

In The Work-Standard (2nd Ed.), the concept of the SSE (Socialist Student Economy) provides clearer definitions on how the Student–the “Self”–defines their own future. The Entry entitled “The State’s Educational Policies and Ranking System” identified four specific areas where they will take their education with them in search of Meaningful Work. Those four are the Council State, Vocational Civil Service (VCS) Economy, Student Government, and the armed forces:

- For Students interested in graduating immediately, they are welcome to join the Vocational Civil Service (VCS) to begin their Vocations in the VCS Economy or Council State, the latter of which will include the armed forces, emergency and social service professions as one of their viable options.

- For Students not interested in graduating, they are allowed to continue their education into the tertiary level by enrolling in the University, its educational curriculum building upon everything that was learned previously at the secondary level.

- For Students still undecided on what their Vocation shall be and have yet to join the VCS, the State or continue their education at the tertiary level, they are entitled to receive a Draft Card from the State and be conscripted into either the workforces or the armed forces.

- The rest of the Student Body will be deepening their overall participation in the SSE by engaging in the political-economic, socio-cultural, military-industrial, diplomatic and educational functions of their “Student Government.” Even working and studying abroad is also covered under this particular category.

From one or more of those areas, the Student will become fully employed as a formal participant in the metaphysical State of Total Mobilization. In the State of Total Mobilization, what is the Student bound to receive from the Council State, beginning from their secondary school years and throughout the course of their lifetime?

Starting in their secondary school years, the Student will their two most important items as part of their rite of passage into adulthood, their Social Rank and first Paygrade (which is given to them as part of their education). The Social Rank is what allows the Student to receive medals, decorations, commendations, promotions and prizes from the Council State. Depending on which Profession they chose for their Vocation, and this can begin as early as their secondary school years, they may become entitled to receiving an additional Stipend from the Council State. The Student may also apply for other important documentation like licenses and permits, passport, party membership papers, technical patents, Profession-related certificates, medical and financial records. For financial records, that can include NSFIs (National-Socialized Financial Instruments), Work-Tenures–interest-free loans borrowed from National-Socialized Banks (NSBs), payment cards (for arranging digital purchases on the national Intranet or international Internet), and others which cannot otherwise be included in personal Paygrades or Stipends.

All of these do sound great on paper, but one might become curious to find out that Pensions are more or less ignored in The Work-Standard (2nd Ed.). Whenever Pensions are mentioned therein, they were always treated as though they were part of the Welfare Capitalist framework, their status befitting of a Social-Democracy than Pure Socialism. Thus, elderly retirees, preadolescent children, and the disabled are included in any given Paygrade as “Dependents.” Similar to married couples, the Geld normally given to them as part of their own Paygrades are combined with that of their household, their family and next of kin or any guardians and caregivers.

What, if any, are the justifications behind the rejection of Pensions as a form of Welfare Capitalism? Could it be that it has more to do with the inefficiencies of conventional Taxation Policies in most Liberal Capitalist regimes?

To begin, it is important for readers below retirement age to understand the significance of Pensions. A Pension refers to the Quantity of Kapital that is put into an account throughout the duration of a recipient’s employment. The Quantity of Schuld comes from the same Quantity of Kapital that the recipient is expecting to be there when they retire, hence the recipient’s status as a ‘retiree’ or ‘pensioner’. Under the Incentives of Supply and Demand, the Pensions of most countries can be organized into a set of Pillars that have much to do with a social safety net to keep people from seriously entertaining Pure Socialism:

- Pillar 1: Publicly-Funded Pension Plan. The “Public Pensions” are funded by the Market/Mixed Economy and redistributed to pensioners by the Parliament through a combination of Taxation and Welfare Policies. Their Incentive is to provide pensioners with a fixed Quantity of Kapital once they reach the mandated retirement age set by the Parliament. Given the inherent problems of Parliamentary Democracy, these Pensions will always be targeted for some form of Privatization or cost-cutting measures due to the sheer expenses of maintaining that social safety net.

- Pillar 2: Privately-Funded Pension Plan. To offset the burdens of the social safety net, a Liberal Capitalist regime will have a secondary Pension Plan for pensioners. These “Private Pensions” are usually funded by a privatized commercial firm and are related to employment with said firm. The Pensions will sometimes be invested into the financial markets on the expectation that the rates of Kapital Accumulation from the financial markets will allow such Pensions to have a greater Quantity of Kapital. Since the Pensions are technically investments in the financial markets, they can be wiped out in the event of an economic or financial crisis. Similar to the ones found in Pillar 1, the Pensions of Pillar 2 are also liable to Taxation.

- Pillar 3: Personally-Funded Pension Plan. Pensions which are funded entirely by the Individual who owns a given Quantity of Kapital. It will be the Kapital that they had generated for themselves as part of their employment and the Schuld will be there for them when they retire. The Schuld here is also associated with Taxation just like the Pensions discussed in Pillar 2, not to mention the penalties of taking Kapital out of a Pension Plan to make immediate payments.

In the State of Total Mobilization, the Pillars correspond neatly to the Freedom-Security Dialectic. The Freedom-Security Dialectic here stems from the roles of Kapital and Schuld. It refers to the unfreedom of losing Kapital in return for the security of gaining Kapital later. Conversely, the insecurity related to the Schuld of having to maintain the social safety net is tempered by the freedom of having younger generations pay the Schuld. Put another way, this is another aspect of the generational wealth gap between the “Baby Boomers” and “Generation X” on the one hand and the “Millennials” and “Generation Z” on the other.

The Pillars also align with the Liberal Capitalist conception of Property, “Common Property” and “Private Property.” If Pillar 1 is represented as ‘Common Property’, then Pillars 2 and 3 reflect two ‘Private Properties’. However, as stated in The Work-Standard (2nd Ed.), the Liberal Capitalist conception of ‘Property’ is always psychically and psychologically understood as Common Wealth (hence ‘Commonwealth’) and Private Wealth. Only in this sense does the Liberal Capitalist conception of Property become apparent in three aforementioned Pillars of Pension Plans.

Given that Kapital and Schuld are both at play in all three Pension Plans, where does the role of Taxation Policy become apparent? How does this influence the manners in which such Pension Plans are financed by most Liberal Capitalist regimes? There are at least three well-known types of payment methods, “Unfunded,” “Pre-Funded” and “Contributed.” Recall what was written earlier about Pension Plans in relation to the Freedom-Security Dialectic because they are reflected in their financing.

Most Pension Plans are Unfunded, relying on a PAYGO (Pay-as-You-Go) arrangement where the Schuld of the Pension must be paid through direct payments and taxes. This is the aforementioned unfreedom of losing Kapital and the security of gaining Kapital later on. The Kapital Accumulation, in addition to direct payments and taxes, can be generated from Liberal Capitalist Financial Instruments (LCFIs) at the financial markets.

Privately and Personally-funded Pensions are more likely to be Pre-Funded or Contributed insofar as the employees of a commercial firm or the Individual (in the case of the Contributed payment method) put a fixed Quantity of Kapital into a privatized Pension Fund. The insecurity and freedom of such an arrangement stems from the fact that there are no guarantees whatsoever that the Quantity of Kapital will be enough for everyone. This explains why business professionals known as “Actuaries” are needed to oversee and evaluate the financing of these Pensions.

Regardless of how somebody pays a Pension or which type of Pension is being discussed, the metaphysics remains constant. In essence, a fixed Quantity of Kapital is set aside somewhere, allow Kapital Accumulation to occur over the course of a lifetime, and to be spent in retirement. The Quantity of Schuld stems from the expectation that there will be a fixed Quantity of Kapital in existence, including the willingness to finance the Pension.

True to the Freedom-Security Dialectic, the very concept of “Social Security” in these United States is no different. There are plenty of Americans who do become surprised by the notion that any Kapital earned from Social Security Income is liable for Income Taxation. American Pension Plans are interesting inasmuch as they are oftentimes hidden behind peculiar designations: “IRAs (Individual Retirement Arrangements),” “401(k)s” (the formal designation for Privately-Funded Pensions, named in reference to subsection 401(k) of the Internal Revenue Code), and “403(b)s” (Internal Revenue Code designation for Pensions reserved to specific Professions like teaching or nursing). What is really interesting is that American Pension Plans are designed in such a manner where Taxation cannot be levied against specific Pensions such as the aforementioned 403(b)s.

If one looks beyond the designations, the organization of American Pension Plans are very similar to those found in European Pension Plans. Individual Retirement Arrangements (IRAs) are related to Pillar 1, whereas 401(k)s and 403(b)s are for Pillars 2 and 3. The only real difference is that American Pension Plans rely on a multitude of Taxation Policy laws designed by the Jeffersonians of the Democratic-Republican Party to complicate the whole Pension process. One cannot help but imagine the possibility that such arrangements create unnecessary inefficiencies all because these American Pensions are subject to Income Taxation.

In the next half of this post, we will discuss about the peculiarities of the American Pension Plans, and how it distinguishes itself from the European Pension Plans found in most EU/NATO member-states. As stated earlier, the most important differences with American Pensions are related to the historical question of Taxation in US History. For those interested in reading more about what The Work-Standard had to write, I am including a link to Part I, Part II, and Part III of SMP Compendium Entry “Taxation and the Work-Standard.”

Categories: Financial Warfare

Leave a comment