The US Pension System was as much a product of American Federalism as it was a product of wartime conditions. This is significant as European-style Pension Systems were the byproduct of Social-Democrats who successfully agitated for such measures, as was the case in Prussia, when half of the German-speaking world was unified into Germany in the 1870s. Thus, unlike the European versions, the US Pension System can split into Federal, State, and Private Pensions. All three were shaped by the Revolutionary War, the Civil War, and the two World Wars.

The historical origins of the first US Pensions can be traced back to the Revolutionary War, inspired by the original Pensions issued to Roman soldiers of the old Roman Empire. American Pensions issued in the Revolutionary War were specifically intended for wartime purposes, awarded to soldiers and sailors fighting on the side of the Thirteen Colonies. Included in these allotted Pensions were war widows and orphans as well as those who became physically disabled. Not everyone who fought were able to receive a Pension, however, because Congress also employed the Pensions to deter desertions and boost morale. The morale boost comes from the personal assurance that if one was to die, their family members will be able to live on without them. The first series of Pensions were issued on August 26, 1776, followed by a second series on May 15, 1778, and then a third series on August 24, 1780.

The US Pension System grew up alongside American Federalism, its historical development a mere reflection of American Federalism’s historical circumstances. The Pensions issued after the Revolutionary War came from both the States and the Federal government. Sometimes, the Pensions were allotments of land that a surviving veteran could have his future home built and the surrounding land converted into farmland. It was not until 1818 that Congress made issuances of Pensions formalized, allowing veterans to receive Pensions for the rest of their foreseeable lives. This law was later amended twice in 1820 and 1822 before including all enlisted and officers by 1832. Today, Revolutionary War Pensions are valued among genealogists interested in tracing someone ancestral ties to the Americans who had fought in the Revolutionary War.

“There was not just one pension system put in place after the war. Union soldiers were covered under the federal system while each former Confederate state had to create and fund its own pension system. And in a change from previous conflicts, it was not only white male veterans who were covered. African American veterans on the Union side were eligible for pensions from the very beginning. Women were also included both as widows and as veterans (primarily nurses) as time went on. Orphaned children were also eligible for assistance although the process was daunting. Each category had its own set of eligibility rules and benefit limits that changed dramatically over time and affected politics on both sides of the Mason-Dixon Line.

For Union soldiers, the pension system began in 1862. Soldiers who were disabled as a result of their service were eligible for pensions; the amount depended on their rank and their injury. Dependents (widows and children) of soldiers who were killed on duty were also eligible. No one got rich from these early pensions. A ‘totally disabled’ private received just $8/month from the first pension system. But amounts increased as it became necessary to recruit soldiers to a war that was no longer popular or easy, and pensions served as recruiting tools.

These first recipients only received benefits from the time of their application. That rule changed in 1879 with the passage of the Arrears Act. The Arrears Act provided veterans a lump sum payment to cover the time between when they left the military and when they applied for the pension. It resulted in both an increase in the number of pensioners and in the amount being expended on pensions. However, the veteran still had to have been disabled as a result of his time in the service. As time moved on the veterans and their families needed more and more assistance, even if they had survived the war relatively intact.

The biggest single change to the pension system came in 1890 with the Dependent Pension Act. Because most veterans did some kind of manual labor to support themselves and their families, and their ability to do so declined over time, political pressure for more help increased (as did the public pleading and private, desperate letters). The 1890 Act expanded eligibility to veterans who were disabled and unable to do manual labor even if that disability was not a direct result of the war. They just had to have served ninety days and been honorably discharged. The result was a huge increase in expenditures and numbers of veterans receiving a pension. More than a million men were on the pension rolls by 1893 and pensions ate more than 40% of the federal government’s revenue. One of the side effects of this legislation was a large number of men transferring their pensions from their previous disability pensions to these new service pensions because the new pensions paid more.”

Recall when I stated earlier that Revolutionary War-era Pensions were prized by genealogists for tracing someone’s ancestry back to the Revolutionary War. In a twist of irony, Civil War-era Pensions have been issued by the Federal government across generations over the course of centuries. Thanks to access to greater access to medicine and healthier foods, anyone who had fought in the Civil War in their twenties or thirties could live as late as the 1950s, when the Civil Rights Movement was gaining momentum. A direct descendant of somebody who had fought in the Civil War was technically eligible to receive Pensions. This is the extraordinary case of Irene Triplett, a ninety year old woman who received $73.13 USD in Pensions before passing away in a North Carolinian nursing home on May 31, 2020. She was the daughter of an elderly Civil War veteran who managed to conceive her in the 1920s, when he was in his eighties. I am including a link to the story for those interested in reading further about this woman.

If the Federal and State Pensions were products of the Revolutionary and Civil Wars, then Private Pensions are products of conditions between the Civil War and the two World Wars. Private Pensions were at first treated as bonus payments to employees of commercial banks and railroad companies in the late 19th century, both of which could afford them in large amounts and to as many people. It was not until the early 20th century that Corporate America began issuing Private Pensions on a more regular basis, and an argument can be made that Income Taxation, as codified in Amendment XVI, played an important role in making the practice commonplace. Any privatized commercial firm that puts Kapital into a Private Pension was eligible to have it be considered exempt from Income Taxation, which was certainly the case with the passing of the Internal Revenue Act of 1921.

Those who have read Part II of “Taxation and the Work-Standard” should remember that Income Taxation in the US was justified under wartime conditions. It was never meant to be a way to ‘redistribute’ the Quantity of Kapital between different segments of the US population. Thus, if the Income Taxation was introduced in World War I, then idea of a Tax-exempted Private Pension became widely popularized by labor unions in World War II. In the latter conflict, the labor unions exploited Tax-exempted Private Pensions as a way to circumvent the Wage Controls that essentially limited their Quantity of Kapital in wages to a fixed amount. Since Pensions were a wartime measure and could not taxed as easily as wages, the labor unions took advantage of those considerations, and this accounts for half of the Incentive behind why the US Pension System had to become a labyrinthine maze.

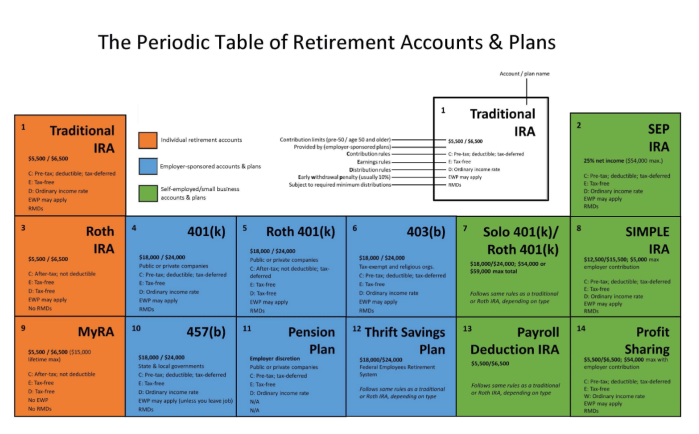

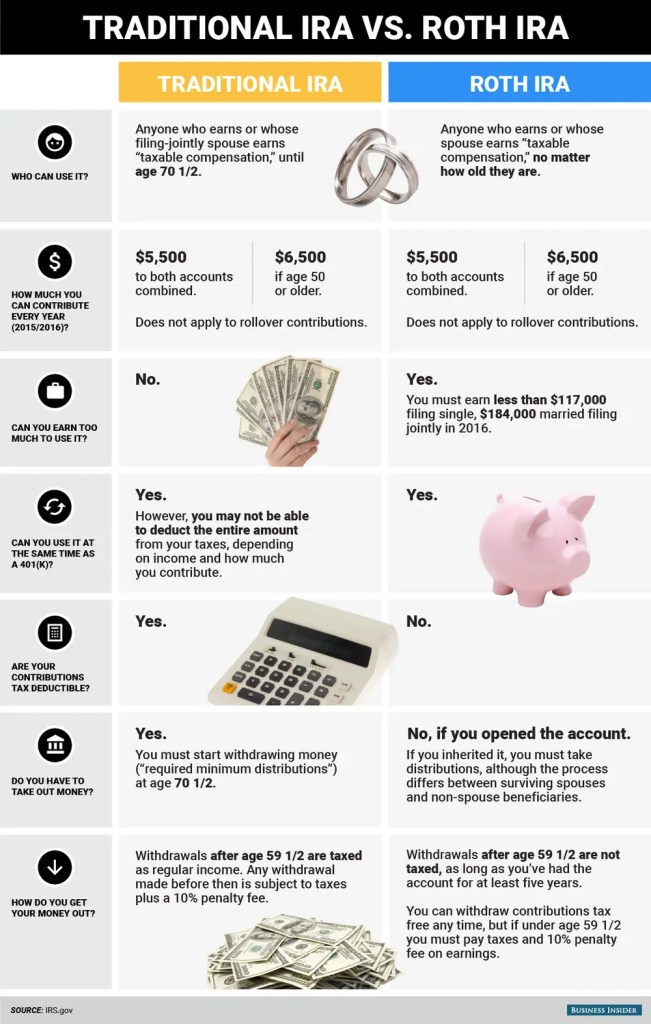

And because the Cold War is a legal continuation of World War II under another name, the second other half of Private Pensions occurred in the 1970s, 1980s, and 1990s. In the midst of tax-cutting measures introduced by Supply-Side Economics, the Tax-exempted Private Pension adopted addition permutations. The “Traditional IRA,” implemented in 1974, and the “401(k)” became a new way to get as much Kapital as possible before one reaches retirement and with the least amount of Income Taxes levied against it. This sort of thinking eventually gave rise to a subvariant called the “Roth IRA,” which was named after Delaware Senator William Roth, who advocated in favor of it in the Taxpayer Relief Act of 1997.

All of these historical events have contributed to why the US Pension System ended up having so many variations of different Pensions. If the first Pensions were issued by the Federal government vis-à-vis the constitutional powers vested into Congress, then could it be that the State and Private Pensions are the consequence of historical ambiguities related to Taxation, the National Debt, and the powers delegated between Federal and State governments? Is it also possible that the Pension System itself helped contribute to why the US capital is Washington DC and not Philadelphia? US History seems to point toward this possibility, as the Pennsylvania Mutiny of 1783 was caused by the issue of not only the need to compensate veterans for their selfless sacrifices, but also who in the Union has the command authority to issue such Pensions:

“During the two years between the Yorktown victory and the signing of the Treaty of Paris in September 1783, the Continental Army and associated state militias remained on duty far from their homes. Many troops awaited back-pay. Finance Superintendent Robert Morris had advised the Continental Congress that it might take years to sort through the accounts of the national and state governments to settle all the claims and payments. Congress passed legislation allowing soldiers to resume civilian life to make a living while the government put its ledgers in order. To allay suspicion that Congress wanted to just forget the army, General Washington announced that all furloughs would be voluntary.

John Dickinson represented both Pennsylvania and Delaware over the course of his time in the Continental Congress. As a Delegate from Delaware, he signed the Constitution in 1787.

Pennsylvania state militias based in Lancaster and Philadelphia were among the unhappiest. They complained that Pennsylvania’s state government, headed by an executive council and its president, John Dickinson, were not paying them. News of the furlough spurred a protest for back pay and discharge dates. On June 20, 1783, about 80 Lancaster officers and militia mutinied and marched toward Philadelphia where they planned to join fellow soldiers. Dickinson and his Council expected their arrival the next day, a Saturday, and prepared to negotiate with them. Dickinson did not worry about the Congress’s safety since it was not meeting that weekend. He planned to meet with the mutiny leaders in his chambers on the floor above the hall of the Confederation Congress.”

Many questions still loom over this historical scrutiny of the US Pension System, all of which can be articulated with a Hamiltonian Federalist Socialist Weltanschauung in mind. Who really pays the US armed forces? Is it the Union (through the Federal government) or the States (through the State governments)? And how would the Federalist American Union address the fundamental flaws and inefficiencies of the US Pension System?

In The Work-Standard (2nd Ed.), I argued in favor of eliminating Income Taxation through a repeal of Amendment XVI, which should only be done once a new Currency pegged to the Work-Standard has been issued and the United States Dollar (USD) replaced with the proposed United States Note (USN). The next step will be to introduce an entirely different system of payments modeled around the Unified Federal-State Civil Service System and the Unified Federal-State Tournament System. A single Paygrade must be enough to cover the living expenses of the elderly, disabled, widows and orphans, all of whom will be counted as the dependents of somebody who is legally responsible for their well-being. This will have to be someone that those dependents know and whom they have grown to trust, like other siblings, cousins, distant relatives, friends, neighbors, confidants, and so forth.

And even then, there will still be social services tasked with assisting these people as part of their dependent status. It would be wise for such services to be brought under the oversight of State governments, but have the actual administering and activities be conducted by organizations working with the Municipal governments. The Federal-State System described in The Work-Standard (2nd Ed.) is specifically designed to incorporate religious and charity organizations into this framework, so they will be working under the local Municipal government’s tutelage, which is in turn subordinated by the command authority of the State government above it.

The goal of such an arrangement should be obvious. Even in an America where Pure Socialism reigns, the American Federalism will continue and the questions over which powers are best-delegated to the Federal government, the State governments, or the Municipal governments remain constant. This is unfortunately the problem with most contemporary proposals for any version of Socialism in the US: too many tend to forget that not everything needs to be done by the Federal government and that the States themselves deserve their own roles. Therefore, since the social services of civilians are handled by the State governments, the social services for those serving in the US armed forces fall under the jurisdiction of the Federal government.

The Pension System may have served its purposes for a time, but its growing redundancy as an old holdover of the Anti-Socialist social safety net is becoming more apparent as time passes. With more people in America and the world at large retiring, the proposals I have written here, and The Work-Standard (2nd Ed.) will become easier to entertain and less extreme in the coming decades.

Categories: Politics

Leave a comment