It should be noted that the LER Process and the Taxation Rate set by the central government are in fact two different sources of wealth. Whereas the Actual Geld in the LER Process originated from the preceding conversion as Actual Arbeit, any Taxation Rate under the Work-Standard will be occurring outside of the LER Process itself. In the context of alcohol beverages, the associated Excise Tax is concerned with their transactional sales. The distilleries and breweries raise the Prices of their products, passing the higher cost to those who intend to drink. The Actual Geld generated from the Excise Taxes are in turn added to the State Budget vis-à-vis the State Revenue:

State Budget = State Revenue – State Expense

Granted, that is only a simplification of what was discussed in The Work-Standard (2nd Ed.). Exactly how the Excise Tax is included to the State Budget by way of the Real Total Financial Potential (RTFP) variable is beyond the focus of this post. But if there is anything that one must always bear in mind, it is that the Work-Standard places far less importance on taxation policy.

Even so, there are a number of interesting tidbits which caught my attention while reading about a recent decision by the Japanese tax authorities regarding alcohol consumption. For those who do not know, alcohol in post-1945 Japan is cheap by Western standards. Here in America, the organizational structure of the Federal-State System enables both Federal and State governments to levy two separate taxes on the sale of alcohol. Meanwhile in Japan, there is only a single tax and it is a “Consumption Tax.” Most Consumption Taxes tend to be levied in the forms of Sales Taxes (a tax on the transaction) or Value-Added Taxes (a tax on a production process).

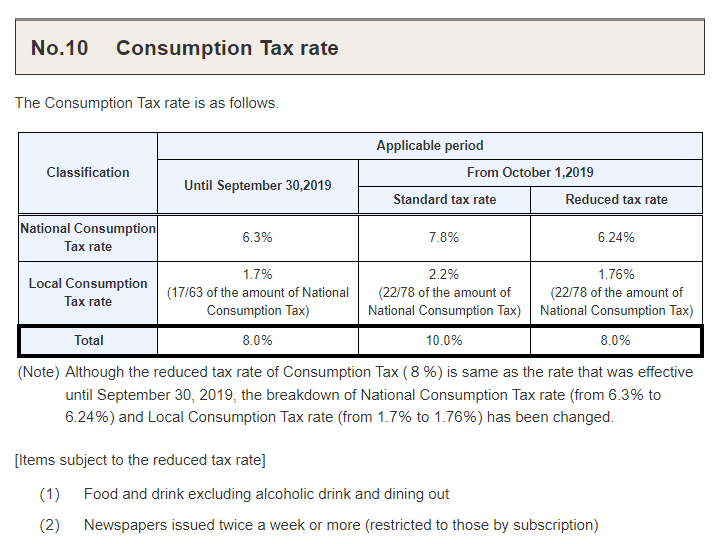

The following photo is a reproduced copy of No. 10 of the Japanese Consumption Tax as it is covered by the National Tax Agency:

Unfortunately for the Japanese government, more than half of their young people are deciding to stay sober instead of spending Kapital on alcoholic beverages. Although the growing decision to abstain from drinking altogether will no doubt be beneficial for the health of their young people, the Quantity of Kapital generated from taxing alcohol consumption is shrinking. It seems that it has gotten to the point in which the National Tax Agency has been looking for ways to ‘Incentivize’ young people to consume more alcohol.

From the standpoint of the Work-Standard, such behavior validates the longstanding conclusion about Production for Profit concerning economic policy: of the four methods that a Parliament uses to finance itself, Taxation is always considered to be the most common. Since the Japanese government cannot afford to raise its Consumption Tax any further, the only logical solution within the framework of Production for Profit is to find ways to increase alcohol consumption. This in turn explains the decision on the part of the Japanese tax authorities to come up with an elaborate contest that is still ongoing as of late.

There is an article from last week in Japan Times, a well-known Japanese news publication, that described the criticism toward the National Tax Agency’s decision on Social Media. For a short article, a few relevant passages do stand out to me as far as the Work-Standard is concerned:

“The National Tax Agency’s ‘Sake Viva!’ idea competition, which is seeking business plans from young people or groups to help ‘revitalize’ the nation’s liquor industry, was launched in July and gained traction on Twitter this week after local and overseas media outlets reported the move.

Brewers in the country have struggled to halt a decline in alcohol sales due to more health-conscious consumers, an aging society and changing tastes among the young. A sharp fall in alcohol sales at restaurants and bars during the COVID-19 pandemic has seen producers resort to promoting more low-alcohol products, while rising inflation is further squeezing profits.”

Aside from younger generations abstaining and the usual demographic concern, we can read between the lines that the decline in alcohol sales during the Coronavirus Pandemic and rising Inflation Rate for the Japanese Yen were the real “Incentives” on the National Tax Agency’s part. But there were other “Incentives” that influenced the rest of the Japanese government, namely the fact that the country has the highest Sovereign Schuld in the world and dealing with the consequences of resorting to Keynesian-like overspending in response to the Lost Decades.

“Japan collected about ¥1.1 trillion in tax from liquor sales, or around 2% of total tax revenue in fiscal 2020, down 13% from 2016, according to tax agency data. The volume of alcohol taxed has steadily shrunk to 7.7 billion liters as of 2020, down nearly 10% from a decade ago, estimates from the tax agency show.

Already saddled with the largest debt burden in the industrialized world, Prime Minister Fumio Kishida’s government has been struggling to rein in spending while tending to the rising demands of an aging population. Earlier this year, the government loosened its commitment to balance its budget by the end of fiscal 2025.”

But if there is something that bothers me, it is the fact that the Japanese government is willing to harness the emerging Artificial Intelligence technologies to enhance the Incentivization of alcohol consumption. Even though I have no information on the extent to which the Japanese government is willing to go, it is concerning because of questions surrounding Surveillance Capitalism. If privatized commercial firms can get away with creating Algorithm-generated advertisements whose personalization is derived from somebody’s personal information, it is not too long before Artificial Intelligence comes along and starts automating the whole endeavor. After including the world’s third-largest economy (by Liberal Capitalist standards) and its Parliament seeking to increase the Quantity of Kapital from a Consumption Tax on alcohol, one cannot help but wonder whether this marks the first steps toward governmental mass surveillance for other purposes besides personalized advertising.

Categories: Economic History

Leave a comment