Economic organizations and Parliaments in Production for Profit or Production for Utility tend to rely on one of two accounting techniques. Those are the “Cash-Basis Accounting Method” and the “Full Accrual Accounting Method.” Both techniques are employed to determine the Quantity of Kapital and Quantity of Schuld as well as to identify their sources. While the transactions are going to be recorded, no Kapital or Schuld will be received until an economic activity has been committed to render goods or services.

In the Cash-Basis Method, the Revenues are recorded by the accountant as the Quantity of Kapital. Kapital is received from the provision of a good or service in a transaction. Likewise, the Expenses are recorded as the Quantity of Schuld. Schuld is created from providing a good or service within the aforementioned transaction as part of that economic activity.

The best way to understand the Cash-Basis Method is to think of it as being akin to a person’s checking account in the Fractional-Reserve Banking System. The Civil Society of a Liberal Capitalist regime maintains the checking accounts of its Private Citizens within the Fractional-Reserve Banking System. Take the Kapital earned from Revenues to find the sum of an account as that Kapital becomes available. Conversely, deduct the Kapital from Revenue as soon as Schuld becomes available.

In the Full Accrual Method, Revenues are only recorded when Kapital has actually been transferred to the economic organization providing a good or service within a transaction as part of an economic activity. The Quantity of Schuld, as Expenses, is revealed as “financial obligations” that must be paid back in full. In essence, all Revenues are accounted for, regardless whether the Kapital has been transferred across the Fractional-Reserve Banking System.

The biggest distinction for the Full Accrual Method is that the Kapital is recorded before it has been received by the economic organization rendering any given good or service. Suppose that somebody had sent a fixed amount of Kapital to a privatized commercial firm in order to pay a bill in exchange for continuing to receive a service. Any Kapital sent to that privatized commercial firm will be recorded in its financial ledger, documenting that they will be receiving Kapital from someone as one of their Revenue sources. If there is any Schuld, it will also be automatically included.

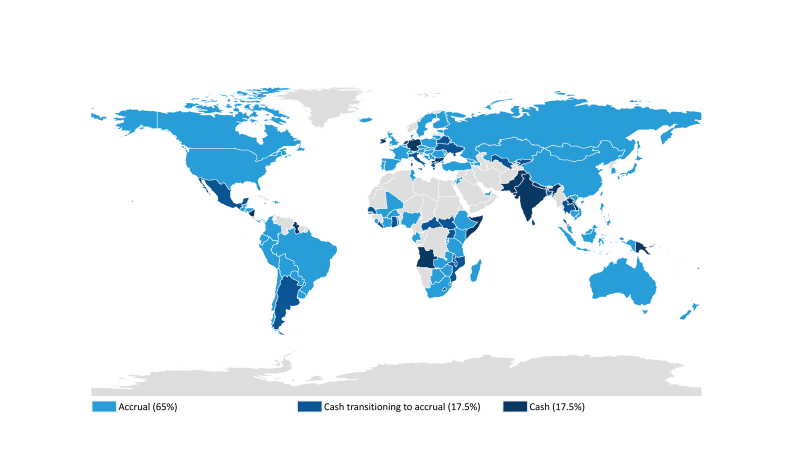

By Liberal Capitalist accounting standards, which of those two techniques would be considered as the most accurate and thus the most used in Double-Entry Account Bookkeeping? If one assumed that it was the Cash-Basis Method, then one would be sorely mistaken. Most economic organizations and Parliaments rely on the Full Accrual Method in order to acquire timely, reliable financial data from their own economic activities. For Parliaments, the Full Accrual Method enables them to process all transfers of Kapital and Schuld ahead of time due to the “financial obligation” attached to a rendering of a good or service. Whosoever provides the good or service becomes legally obliged to provide that good or service, making the Full Accrual Method ideal for collecting taxes and allocating investments.

However, it should be noted that not all Parliaments rely on the Full Accrual Method. For the purposes of budgeting, some tend to employ the Cash-Basis Method.

In the contexts of Production for Profit and Production for Utility, the Full Accrual Method is most compatible with Production for Profit. The Full Accrual Method enables the accountant to balance the Quantity of Kapital and the Quantity of Schuld to discover the true values of Assets, Liabilities, and Equities. The same could be said for the Cash-Basis Method, which explains why it is understandable to expect certain Parliaments to employ the Cash-Basis Method and others to rely on the Full Accrual Method. After all, the key differences distinguishing the two accounting techniques is precisely where it becomes necessary for Kapital and Schuld to be recorded on the financial ledger and when Kapital and Schuld should be processed as part of a given transaction.

If the Cash-Basis Method and the Full Accrual Method are applicable to Production for Profit, what can be said about Production for Utility? Two other accounting techniques have been employed, which are the “Modified Accrual Method” and what can be described as a “Hybrid Method.” Over the course of the next Entry, we will explore those two and how they in turn differ from the accounting techniques described here.

Categories: Work-Standard Accounting Practices

Leave a comment