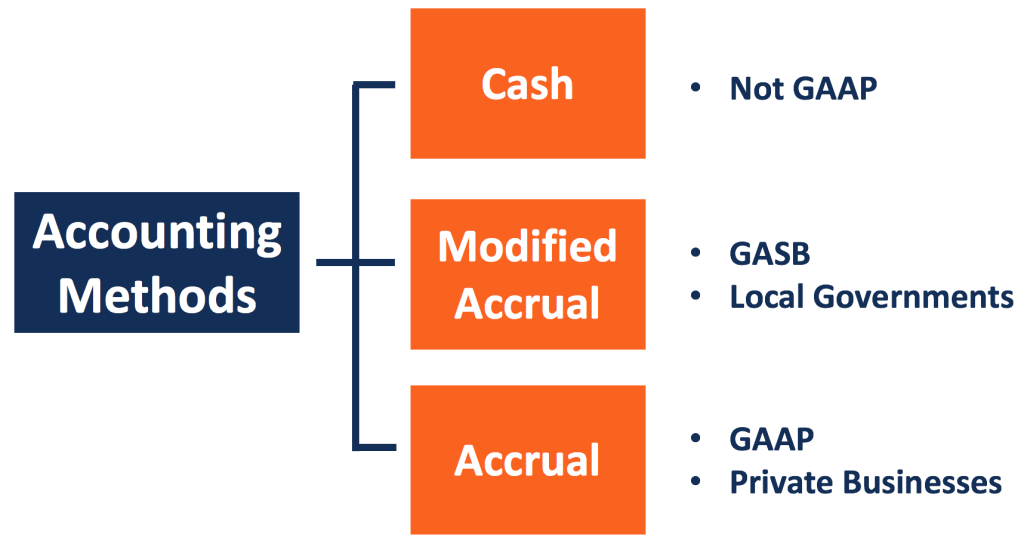

Economic organizations operating in Production for Utility may record their economic activities with the “Modified Accrual Method.” The Modified Accrual Method is a combination of the two aforementioned accounting techniques discussed in the previous Entry, the Cash-Basis Method and the Full Accrual Method. In terms of applications, the Modified Accrual Method is similar to the Cash-Basis Method, albeit with the intended functions of the Full Accrual Method. What distinguishes it from the other two accounting techniques is how the Quantity of Kapital and Quantity of Schuld are recorded and processed by accountants assigned to economic organizations whose Mode of Production is Production for Utility.

An accountant would record the transactions of economic activities as soon as Kapital and Schuld become “measurable” and “available.” By “measurable,” the Quantity of Kapital denoted as Revenue should be given reasonable estimations. And by “available,” the Quantity of Kapital itself should also be enough to pay off any outstanding Quantity of Schuld as Expenses within the next sixty to one hundred twenty (60-120) days. The justification for this accounting technique is to account for any Kapital donated to non-profit economic organizations in the “Public Sector,” which is to say Kapital accumulated from economic activities in Production for Utility. Any Kapital donated to economic organizations operating in Production for Utility needs to be recorded and processed by the accountants even though the Kapital itself is going to be immediately obtained by the receiving economic organizations.

Such parameters are made feasible because of the fact that the Quantity of Kapital and the means by which the economic organization receives the Kapital is readily known to the accountant in their financial ledger. Similar to the Full Accrual Method, the Modified Accrual Method has “financial obligations” attached to all Kapital and Schuld in every transaction. This means that the Quantity of Schuld itself does not appear until somebody voluntarily agrees in principle to spend Kapital on behalf of an economic organization operating in Production for Utility.

Furthermore, it is possible for certain Liberal Capitalist regimes to employ a “Hybrid Method,” which involves employing a combination of the Cash-Basis Method, the Modified Accrual Method and/or the Full Accrual Method. Certain sources of Kapital and Schuld would be recorded using the Cash-Basis Method, whereas other sources are recorded with the Modified Accrual Method. This arrangement becomes relevant in a Liberal Capitalist regime where the delicate paradigm between Production for Profit and Production for Utility is at its most apparent. It is possible to encounter the Parliament itself employing the Cash-Basis Method, while the local Municipalities subordinate to them are relying on the Modified Accrual Method and/or the Full Accrual Method.

The Hybrid Method and the recent adoptions of the Full Accrual Method across the “Liberal International Economic Order (LIEO)” throughout the early 21st century does raise some important implications for the Work-Standard and its own conceptions of accounting practices. How important is the precise timing in which Kapital and Schuld is processed between the accounts of persons, economic organizations, and governments? Does the timing itself provide subtle indications about Liberal Capitalist conceptions of Currency, the Fractional-Reserve Banking? What about the relationships between Kapital and Schuld as well as Production for Profit and Production for Utility?

In essence, there are accounting techniques within the Double-Entry Account Bookkeeping System that allow someone to record and process the real-time transactions of Kapital and Schuld. One technique is ideal before the rendering of a good or service (Full Accrual Method), another set in the midst of rendering a good or service (Cash-Basis Method), and another for after the rendering of a good or service (Modified Accrual Method). Clearly, someone is not always going to pay the Kapital now, so they will gladly accept the Schuld and pay it off later if it means receiving a good or service.

If so, then the chronological order in which those accounting techniques would become applicable has to look something like this:

Full Accrual >> Hybrid >> Cash-Basis >> Hybrid Method >> Modified Accrual

One cannot help but wonder whether all three accounting techniques are related to the inherent characteristics of the Post-Bretton Woods Debt Standard and the worldwide adoption of Fiat Currencies since the 1970s, not to mention the Fractional-Reserve Banking System. Thanks to Financialization, Globalization, and the Financial Technologies introduced during that same decade, it is now feasible for someone to use a Credit Card to purchase items beyond the Kapital that they already have in exchange for obtaining Schuld. Massive sums of Kapital and Schuld can be created within a very short timeframe by untold numbers of people interacting with their country’s Fractional-Reserve Banking System. The “financial obligations” inherent in both the Full Accrual and Modified Accrual Methods are what makes this analogy entertainable. And because most Kapital and Schuld in existence in the 21st century is not backed by Gold, Silver, or any other tangible “Commodities,” such “financial obligations” can then be easily converted into social control mechanisms through financial means.

The Hybrid Model in particular only reinforces this consideration, seeing how it is a combination of the other three accounting techniques. Not only does it reflect the paradigm shared by Production for Profit and Production for Utility, it also demonstrates how Parliamentary Democracies tend to have different priorities on exactly when they would need Kapital and where they could sustain Schuld as part of their economic policies. There may be a Parliament somewhere in the LIEO that would need an instant inflow of Kapital sooner rather than later in order to balance its Parliamentary Budget. Any Schuld incurred from governing the Liberal Capitalist regime could then be paid off, at least that is how it would appear on paper. Subordinate Municipalities can afford to wait for their Kapital and Schuld, especially if the Parliament itself is allocating Kapital to their governments.

This raises the question of the Fractional-Reserve Banking System, its relation to the aforementioned accounting techniques, and the Fiat Currencies that are being recorded and processed by the accountants. The Kapital and Schuld are abstract enough to not always represent physical units of currency. They are merely numbers on the financial ledger which were given meaning by the accountants and their interactions with the Fractional-Reserve Banking System. For the Fractional-Reserve Banking System, it matters very little whether the units of currency are in banknotes and coins, gold and silver, or digital currencies. What is giving those units of currency its inherent Value and therefore its Price, as Kapital, is Schuld itself.

Here, we come full circle to the question that I had posed in the beginnings of The Work-Standard (2nd Ed.) and The Third Place (1st Ed.): who or what ascribes to any conception of Currency its Value and Price? This sort of question is related to a Theory of Value and a corresponding Theory of Money. What is expected of the accountant is find the true Value and the true Price based on those Theories.

Moreover, the accounting techniques also imply the presences of two important characteristics exhibited by Parliamentary Democracy which ultimately differ from those of Council Democracy:

- A Parliament maintains its own “Parliamentary Budget” where Kapital and Schuld are distributed across a series of “Parliamentary Funds” intended for the budgets of its governmental organizations and any economic organizations under its purview in Production for Utility.

- These Parliamentary Funds have their own sources of Kapital and Schuld, which may or may not necessarily originate from the Parliament itself.

Categories: Work-Standard Accounting Practices

Leave a comment