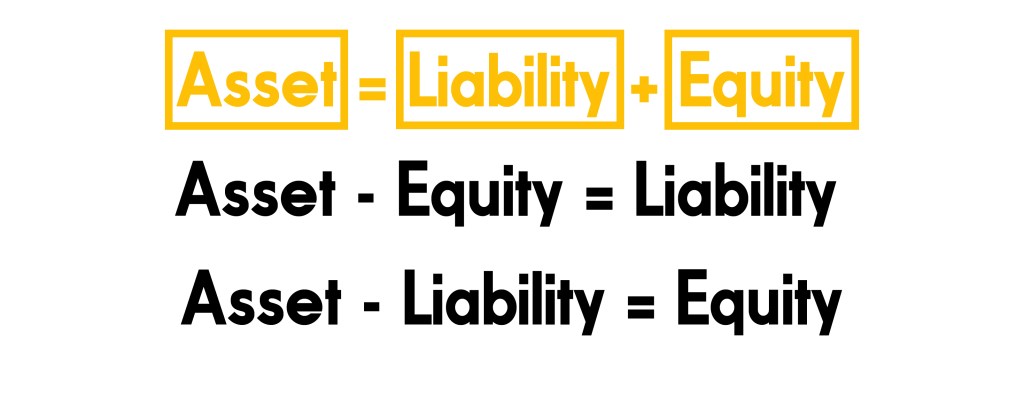

In Double-Entry Account Bookkeeping, the most fundamental equation used to form the basis of all accounting and econometrics under Neoliberalism involves basic addition and subtraction. Practically anyone with a basic primary school education should be able to comprehend the following:

The above equation demonstrates that the “Assets” owned by a Private Citizen or privatized commercial firm represents the sum of all “Liabilities” and “Equities.” How does anyone even begin to fathom the beginnings of a Socialist conception of accounting compatible for the Scientific Socialisms (Marxist Socialisms) and the Artistic Socialisms (Non-Marxist Socialisms)?

It is only a simple arithmetic equation, so there is no point in trying to add anything more complex than that. Therefore, our deviations from Neoliberalism begin with replacing the variables or what is being measured by that equation. What is being measured under the variables “Asset,” “Liability,” and “Equity?”

The “Asset” refers to the Quantity of Kapital that someone or an economic organization possesses in order to create more Kapital. The “Liability” is the Quantity of Schuld that they will accrue over the course of creating new Kapital. The “Equity” denotes the Quantity of Kapital that remains after deducting the existing Quantity of Schuld.

Given the above equation, we can find the Liability from the difference of Asset and Equity or the Equity from the difference of Asset and Liability.

The second equation in particular is required to discover somebody’s Net Worth, which is equal to their Equity. This validates the earlier conclusion about viewing “Asset” and “Liability” as the Quantity of Kapital and the Quantity of Schuld respectively.

After developing familiarity with the basic fundamental equation of the Double-Entry Account Bookkeeping System, we can then determine how much Kapital and Schuld somebody receives as “Revenue,” “Expenses,” and “Drawings.”

Here, Equity is expanded to encompass the existing Quantity of Kapital currently owned by a privatized commercial firm, the Quantity of Kapital earned from transactional sales, the Quantity of Schuld from the creation of new Kapital, and the Quantity of Schuld from removing Kapital for personal Incentives.

By knowing the “Assets,” “Liabilities,” “Equities,” “Revenues,” and “Expenses” of a privatized commercial firm, the “Balance Sheet” of a privatized commercial firm can then be compiled and its “Chart of Accounts (CoA)” established for the Fractional-Reserve Banking System. The Balance Sheet provides a privatized commercial firm with basic information abouts its own finances. The CoA, on the other hand, is a more detailed record documenting every known source of Kapital and Schuld.

Categories: Work-Standard Accounting Practices

Leave a comment