Are there any corresponding financial indicators related to Production for Profit and Production for Utility? If so, are there two separate sets, one for individual economic organizations and another for Parliament? Back in the previous Entry, we discussed the System of National Accounts, and how it was used to convey information about economic performance. The most important aspect is the inputs and outputs of Kapital and Schuld related to production processes and the distributions of income. Such economic indicators are going to be accompanied by corresponding financial indicators, which provide additional information about how those same Quantities of Kapital and Schuld are being earned and spent, saved and invested, loaned and borrowed. The way to approach the question of financial indicators is to identify the ones relevant to individual economic organizations and how they are related to Parliament within Production for Profit and Production for Utility.

Some of the financial indicators used by Parliament have been described in The Work-Standard (2nd Ed.). The Inflation/Deflation Rate, the Interest Rate, and Taxation Rates are three notable examples. There is also the Foreign Direct Investment (FDI), the Sovereign Schuld, and the Exchange Rate. But what was not addressed in that Treatise is that those financial indicators are also capable of affecting the financial indicators employed by for-profit and non-profit firms.

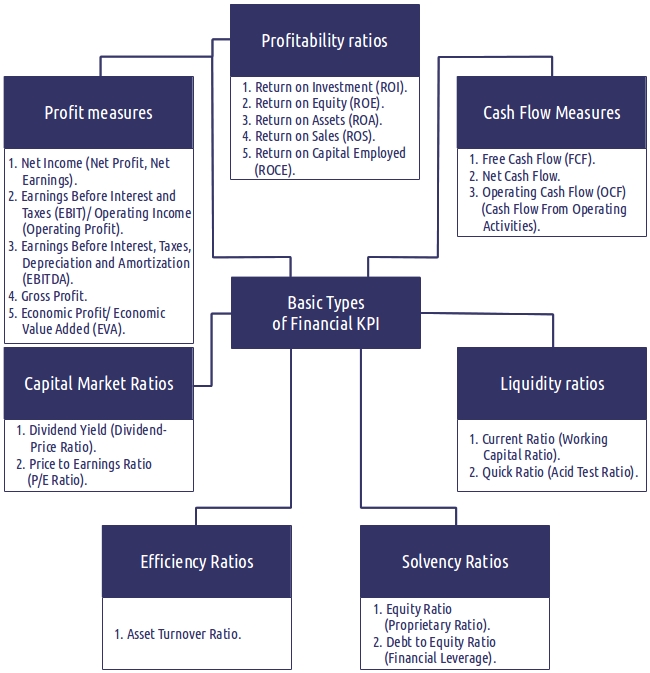

Double-Entry Account Bookkeeping provides the framework for economic organizations in Production for Profit and Production for Utility to uncover financial data about its Kapital and Schuld. “Key Performance Indicators (KPIs)” are employed to identify not only the sources of Kapital and Schuld, but also the costs, expenditures, and expenses of conducting economic activities. The vast majority of KPIs involve using Double-Entry Account Bookkeeping to acquire financial data on how Kapital and Schuld are affecting the Profitability/Utility, Liquidity, Efficiency, Valuation, and Leverage of an economic organization.

Certain indicators govern how much Kapital is accrued from transactional sales as “Earnings Before Interest & Taxes (EBIT),” such as the “Gross Profit Margin” and the “Net Profit Margin.” Some pertain to how well the economic organization is able to sustain its ongoing Liabilities relative to its own existing Assets. Three indicators are concerned with payments for the inputs and outputs of production processes. “Accounts Payable Turnover” records payments for resource inputs from sellers, whereas “Accounts Receivable Turnover” tracks payments for product outputs from buyers. Both are related to the “Inventory Turnover” of resource inputs and product outputs. Other indicators are related to “Debt-to-Equity Ratio,” the Value of Stocks as an LCFI in “Earnings per Share,” while the “Returns on Assets” and “Returns on Equities” depict how well an economic organization was able to profit with the resources that it already has.

Again, the obvious purpose of KPIs as part of a Chart of Accounts (CoAs) is to show how an economic organization is creating Kapital and Schuld from transactional sales. It also demonstrates how that same economic organization contends with the Interest Rate, the Inflation/Deflation Rate, the Unemployment/Employment Rate, Taxation Rates, and meeting its own “financial obligations” to privatized commercial banks and investors at the Financial Market.

But what would be the other purpose of acquiring such data? By gathering enough information on the finances of an economic organization, an accountant would be able to draw conclusions about its financial solvency. They can make projections based on past actions to describe what future awaits the economic organization if present trends continue uninterrupted. They will even be to argue why the budget of that economic organization will be affected by its expenditures and revenues as well as changes to its Assets, Liabilities, and Equities. Every possible conclusion reached by the accountant was made feasible because of the nature of Double-Entry Account Bookkeeping and because it demonstrates the relationship between Kapital and Schuld, Production for Profit and Production for Utility. Moreover, it also confirms that the Fractional-Reserve Banking System supports the Market/Mixed Economy, both of which are responsible for providing the economic and financial firepower wielded by Parliament and Civil Society.

The intended result of receiving financial data from the accountant is that economic organizations within Production for Profit and Production for Utility will be able to reevaluate their past decisions. The KPIs reveal the past decisions of economic organizations, allowing them to deduce how their current decisions as of late will impact their future decisions. In fact, the actions taken in the present may even affect whether the economic organizations themselves will survive over the short term or the long term. Thus, it becomes imperative on the part of those economic organizations to readjust their current decisions to ensure a more desirable outcome for their investors and lenders.

Categories: Work-Standard Accounting Practices

Leave a comment