Since Production for Dasein relies on Command-Obedience Account Bookkeeping and the Reciprocal-Reserve Banking System, it should not be too unusual to expect Financial Reporting practices specifically catering to the Work-Standard. Accountants familiarized with the Worksheet of Sociable Accounts need to be able to convey the financial data on their ledgers through one of three Financial Statements. Those Statements are referred to in Command-Obedience Account Bookkeeping as the WSA’s “Workflow Statement,” “Income Statement,” and “Balance Sheet.” Even though the latter two Financial Statements share the same names as their Double-Entry Accounting and Fractional-Reserve Banking rivals from Neoliberalism, outward appearances are deceiving. In terms of functionality, however, the WSA Income Statement and Balance Sheet operate according to Arbeit and Geld, not Kapital and Schuld.

Visualizing Command-Obedience Account Bookkeeping

If there was an appropriate symbol to convey the accounting practices of the Work-Standard, not to mention a visual for Accountants and non-Accountants alike, it will be this one:

The Symbol itself reflects the cycle of Arbeit contributions and Geld generations by the State, Totality, and Self under the Work-Standard. The Totality and Self constitute the State, just as the State is comprised of the Totality and the Self. This State, be it a Council State or a Corporate State, personifies the State of Total Mobilization, whose appearance marks the true withering of the old State of Natural Rights from the Enlightenment. The wedges inside the Symbol signify the three types of Financial Statements, the Y-Junction signifying the three Principles that govern the LEBM (Life-Energy Basis Method) and NSBM (National-Socialization Basis Method) Techniques within Command-Obedience Account Bookkeeping.

The State of Total Mobilization demands a new-old humanity that shall restore the balance between Self and Totality, Self and Communion, Self and Family, Technology and Nature, Tradition and Innovation, Social Rank and People’s Community, Church and State, Nation and World Order. The Enlightenment’s State of Natural Rights, personified by Neoliberalism, must be allowed to pass away as the very Modernity which has yet to meet its end by the onset of a true Postmodernity after the 20th century. Nothing here should seem Utopian or Dystopian, especially as humanity struggles in search of a new political, economic and social purpose in the wake of two World Wars, of which the Cold War was merely the continuation of the Second World War.

Ten Recurring Figures

As discussed earlier in The Third Place (1st Ed.), in Mission-Type Economic Planning (MTEP), most Enterprises within the SSE and the VCS Economy are going to be encountering ten Figures who bear some relation to their production processes. Those are the “Civil Servant,” the “Delegate,” the “Administrator,” the “Accountant,” the “Economic Planner,” the “Inspector,” the “State Commissar,” the “Superintendent,” the “Central Planner,” and the “Investor.” The three Financial Statements of Command-Obedience Account Bookkeeping are designed to accommodate those ten, regardless of the type of economic organization, Social Ranks of everyone and the economic organization in question within the Tournament, and whether we are talking about a Planned Economy or Command Economy and Council State or Corporate State.

The Civil Servants and Delegates are going to need a Financial Statement that enables them to know how much Arbeit and Geld they are contributing to the Life-Energy Reserve. They will use that information to request periodic alterations to the Paygrade Scale at the State Commissariats.

The Administrator and the Economic Planner require a Financial Statement that would enable them to evaluate the overall performance of their own Enterprise. They need to know how well their Enterprise is living within its own means of production, how they are spending Geld from their State Fund, and the necessary information to request periodic alterations to the Price Scale at the State Commissariats.

The Inspector, Investor and State Commissar rely on Financial Statements to ascertain the Sustainability and Quality of an Enterprise’s production processes. The Inspector routinely audits the Enterprise to ensure that the Civil Servant, Delegate, Administrator, and Economic Planner are exercising accountability and transparency within their economic activities. The State Commissar bears the Command Responsibility of ensuring that all Prices stay within acceptable boundaries in the interests of the Totality and the State. The Investor bases most of their allocations of Arbeit and Geld to the Reciprocal-Reserve Banking System, whether at the Kontore or at the National-Socialized Banks (NSBs), on information provided to them by the Reciprocal-Reserve Banking System vis-à-vis the State Commissariats.

The Superintendent and the Central Planner are not interested in the little details, convinced that this is the Command Responsibility of the others and their own. They prefer their Financial Statements to give them a comprehensive overview of all economic activities across the VCS Economy and the SSE.

In essence, everybody is counting on the Accountant to ensure that their financial ledgers are up-to-date and always recording when possible the known Qualities of Arbeit and Geld from all economic activities. Remember, only economic activities attached to a designated Domain within the Work-World is allowed to be contributing Arbeit and Geld to the Life-Energy Reserve. Anything outside the Domains of the Work-World will be considered illegitimate and therefore subject to scrutiny by the police and the courts.

While studying the three Financial Statements, pay attention to the details, and decide for oneself which one of the three Financial Statements matches the descriptions described above.

Types of WSA Financial Reports

The Workflow Statement describes all of the known sources of Arbeit and Geld associated with a given Enterprise. Every conceivable source is to be consolidated and organized into one of three categories:

- Arbeit-into-Geld Activities: Arbeit and Geld from Production Processes.

- Geld-into-Arbeit Activities: Arbeit and Geld from Transactional Sales.

- National-Socialization Activities: Arbeit and Geld from NSFIs and State Investments.

A Workflow Statement also features information that takes into consideration the movements of Arbeit and Geld both within the Enterprise and without. Note that the production processes of certain Enterprises are intended to ensure that other Enterprises are able to create Arbeit and Geld from their own economic activities. There may be circumstances where the Enterprise may issue Fiefs and Work-Plans, two very common types of NSFIs, to Investors, enhancing their overall Workflow.

Another feature not found in the other two Financial Statement are distinctions between the six main types of Arbeit and Geld discussed earlier in this Treatise. If an Enterprise is contributing more than just Actual Arbeit and Actual Geld, the Workflow Statement is designed to include sources of Digital Arbeit and Digital Geld as well as sources of Military Arbeit and Military Geld. Sources related to the former originate from the National Intranet, whereas those pertaining to the latter stem from the Military-Industrial Complex.

It even includes the Opening Balance and the Closing Balance for a given Fiscal Year (FY). Any changes in the contributions of Arbeit and generations of Geld between the beginning and ends of the Fiscal Year are to be accounted for. The Closing Balances of all Enterprises form the final sum of the Closing Balance for the actual WSA itself, which is equal to the Final TPP Value.

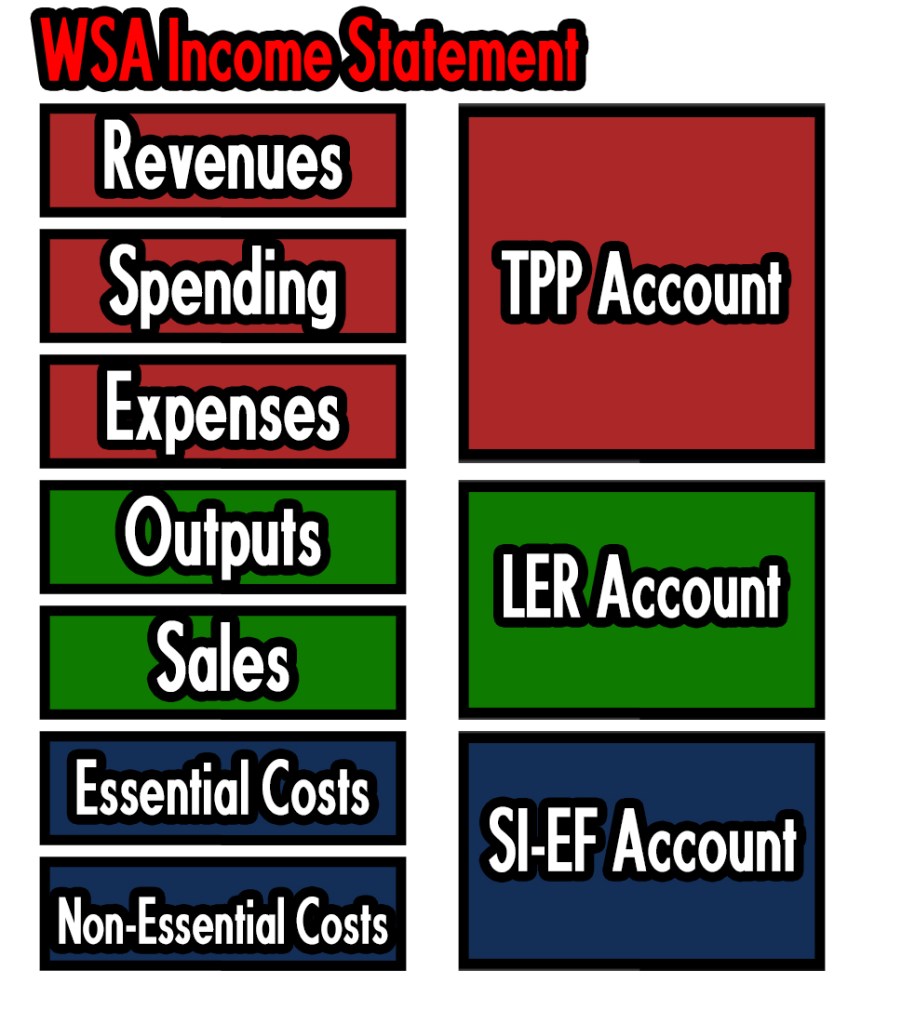

The Income Statement outlines all of the known sources of Revenues and Expenses for an Enterprise. Similar to the Workflow Statement, the Income Statement is formatted into three categories:

- TPP Account: The overall Revenues and Expenses of a given Enterprise.

- LER Account: Revenues and Expenses from economic activities.

- SI-EF Account: Revenues and Expenses required for production processes and transactional sales, followed by Revenues and Expenses from outside of an Enterprise’s production processes and transactional sales.

It tracks how much of the State Fund must be spent on sustaining the production process and transactional sales as well as any Geld received from them. Additional information pertaining to how much Geld is being allocated toward Essential Costs and Non-Essential Costs are also included here as well. The purpose of this Financial Statement is to provide a detailed summary of where and how a given Enterprise obtains its Geld and how it spends that Geld. With that sort of information, one could draw inferences about the Sustainability of the production process and Quality of Arbeit based on that data.

The layout is based on the WSA format for ease of reference and relevance to those who may require that information to make decisions involving the Enterprise in question. One could even draw some well-informed conclusions about its performance among the Social Ranks of the Tournament and how well it compares to other Enterprises within its affiliated Industry and Economic Sector. Pricing data could be drawn from the Income Statement relative to the Attrition/Inaction Rate (AIR), the Mechanization Rate (MR), the Economic Socialization (ES) Rate, and the Solidarity Rate in terms of the Scale and Scope of its production process (SR1 and SR2 respectively).

Compared to the other two Financial Statements, the Balance Sheet is a generalized summarization of how an Enterprise contributed Arbeit and Geld to the Life-Energy Reserve, how much it receives from transactional sales, and how much it of its Arbeit and Geld comes from NSFIs and State Investments. All of the known Revenues and Expenses are consolidated into two sets within three categories pertaining to the three main WSA Accounts:

- TPP Account: The overall of Value of Income that an Enterprise receives from all sources of Arbeit and Geld, how much it has to allocates toward Essential Costs, how much it allocates toward Non-Essential Costs, and how much it receives in Revenue throughout a given Fiscal Year (FY).

- LER Account: The Value of Arbeit and Geld from Production Processes and Transactional Sales, and all known Expenditures associated with each.

- SI-EF Account: The Value of Arbeit and Geld from NSFIs and SI-EFs, and all known Expenditures associated with each.

The Value of the Total Balance in a Balance Sheet should be equal to the Closing Balance within the Workflow Statement. The Value of all Revenues and Expenses should also be equal to their corresponding Values within the Income Statement. Other sources of Revenue and Expenses, such as damages, thefts, wartime or peacetime losses, and so forth must be accounted for as well.

The Balance Sheet will not be able to make distinctions between Actual Arbeit and Actual Geld, Digital Arbeit and Digital Geld, and Military and Military Geld. The combined Values of these types of Arbeit and Geld are consolidated into two separate Values, one for Arbeit, the other for Geld.

Categories: Work-Standard Accounting Practices

Leave a comment