I had previously written about the topic of taxation in The Digital Realm (1st Ed.) within the context of the National Intranet. A brief passage was devoted to it in the “Scenario 1999: International Relations between SSEs and their Central Governments” Entry. The argument that I had posited at the time was that, under the Work-Standard, taxation rates on the National Intranet would be identical to those implemented offline. Any taxes levied by the Council State could be easily reapplied online insofar as the National Intranet was an extension of the national life occurring back in the Real World.

However, I had also written critically of taxation policies that rely on Production for Profit and Production for Utility and reapplying them to the Digital Realm. There have been three variations of taxation policies proposed by Neoliberalism since the 1990s: taxing access to the Digital Realm, Sales Taxes and VATs, and Use Taxes and Digital Services Taxes (DSTs):

Back in Production for Profit and Production for Utility, the proposal from the Liberal Capitalists was for Parliaments to levy taxes either on goods and services sold on the WWW, facilitating access to the digital realm, or treating emails with the same rates as postal mail. While the third proposal was self-explanatory, the first taxation policy is the online equivalent of a Sales Tax or VAT (Value-Added Tax), the second functions similarly to charging tolls and fares. It may seem like an odd idea from hindsight, but the Liberal Capitalists did at one point consider taxing emails back in the 1990s.

More recently, another proposal involved the levying of a “Digital Services Tax (DST)” that would be applicable to foreign privatized commercial firms that do not have a physical presence within a Liberal Capitalist regime. It would also be applicable to those which provide services such as streaming, advertising, software, and overall data usage. When put into practice, a DST would function as a stopgap between the more conventional Sales Taxes and VATs and Corporate Income Taxes.

For the purposes of the Work-Standard, the Council State will not be levying such taxes on the Totality, Student Body or Foreigners. It will also not be charging taxes on Foreigners outside of the terms of an RTA. What the Council State should consider, however, is whether Foreigners should meet a certain Social Rank within their own nations before they could be eligible to access the National Intranet from outside an Internet Café. This question deserves to be left open-ended insofar as there are potential arguments for and against such a proposal if brought to the floor of the State Council within a functioning Council Democracy. The requirement is different from that of the Social Rank prerequisite for acquiring NSFIs (National-Socialized Financial Instruments) because the Kontore expect only the most reliable and dependable Investors. The Investors need to be those whom they can trust and work with over the long term.

As I had been suspecting for years, the Liberal Capitalists have sought to turn the Digital Realm into an extension of Neoliberalism. One example of this has been an attempt at consolidating Production for Profit and Production for Utility in the World Wide Web (WWW). The issue at stake is how to harness the Digital Realm itself for the purpose of Kapital Accumulation vis-a-vis Profit and Utility Maximization. Taxation policy is one of the pressing issues for Parliamentary Democracies interested in earning tax revenue from digitalizing the Market/Mixed Economy.

In America, back in the 1990s, the Jeffersonians under the Clinton Presidency passed the Internet Tax Freedom Act (ITFA) of 1998. The purpose of ITFA was to implement a three-year moratorium on the taxation of American economic activities conducted on the WWW. This meant that neither the Federal government nor the Municipal and State governments could implement their own taxation policies. The idea was to ensure that America would realize a standardized taxation regime, applicable to the entire Union. The justification rested on the Constitution’s “Commerce Clause,” which stipulated that all economic activities related to “interstate commerce” fall under the purview of Federal Law.

The concept of “Commerce Clause,” it should be noted, was observed in The Work-Standard (2nd Ed.) in regard to the delineation of Economic Organizations in the Federal-State System of American Federalism. There are economic activities which are to be governed by the State governments and others to be governed by the Federal government. The Social Ranking System was designed to promote this delineation according to the Intents of Command and Obedience. The largest and most influential Enterprises would be designated as “Federal Enterprises,” followed by the intermediate “State Enterprises” and the lower-ranking “Social Enterprises.” In the Work-Standard, State and Municipal governments could pass their own taxation policies, independent of the Federal government. But it is the Federal government, not the State and Municipal governments, that owned and controlled the American Life-Energy Reserve as part of the US Treasury.

But because the Jeffersonians are incapable of thinking in terms of Arbeit and Geld, the collection of Kapital and Schuld by taxation meant that a number of accounting issues arose. One key challenge that they were concerned about was actually something that I incidentally raised in Work-Standard Accounting Practices (1st Ed.), “Double Counting.” Double Counting occurs when an Account records two entries for a single transaction, when they should only be one entry. “Double Taxation” is a variation of that same problem for taxation policy, where the same Quantity of Kapital is being taxed twice by a single taxation policy.

To illustrate an example, suppose for a moment that someone has $120.00 United States Notes (USN), the American Sociable Currency under the Work-Standard. A State Tax deducted $30.00 USN from that initial figure, followed by $15 USN from a concurring Federal Tax. Rather than having $90 USN left over, the final total is now $75 USN.

Two variations of that same phenomenon occur, one in the Financial Markets of the Fractional-Reserve Banking System, the other in Free Trade Agreements (FTAs). The former comes from paying the Dividends of Stocks to Shareholders because, in Neoliberalism’s conceptions of Legal Jurisprudence, the Privatized Commercial Firm and the Shareholder are two different entities. The latter, on the other hand, involves Privatized Commercial Firms being taxed by their Parliament and either another Parliament (if the other country is Liberal Capitalist) or a Corporate State and Council State (if the other country is not Liberal Capitalist). In each of those cases, there is at least one additional tax. Real World instances of Double Taxation can include multiple instances of taxation on the same source but from different entities. For the Jeffersonians and their Empire of Liberty, the solutions have been to standardize taxation regimes, readjust taxation rates, and sign special “Double Tax Agreements (DTAs)” to complement a coexisting FTA.

Thus, the ITFA of 1998 was intended to prevent the Real World scenario of Federal, State and Municipal governments taxing a single transactional sale. Since the WWW disregards all notions of State Sovereignty and Personal Privacy due to how it was inherently designed, a “Multiple Taxation” on the same Quantity of Kapital became inevitable.

Consider the possibility of an eCommerce transactional sale. A Privatized Commercial Firm in Philadelphia, Pennsylvania is selling a product to customer living in Newark, New Jersey. Without ITFA, it is legally feasible to speak of the Municipal governments of Philadelphia and Newark, the State governments of Pennsylvania and New Jersey, and the Federal government to tax that same transactional sale up to five times in Sales Taxes. It is because of this implication that the Obama Presidency would later permanently sign ITFA into Federal Law as part of the Trade Facilitation and Trade Enforcement Act of 2015.

A few Supreme Court cases over the past ten years have been heard over the constitutionality of ITFA. The rulings of the Supreme Court presented the possibility of challenging the ITFA on constitutional grounds, specifically Amendment X:

“The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.”

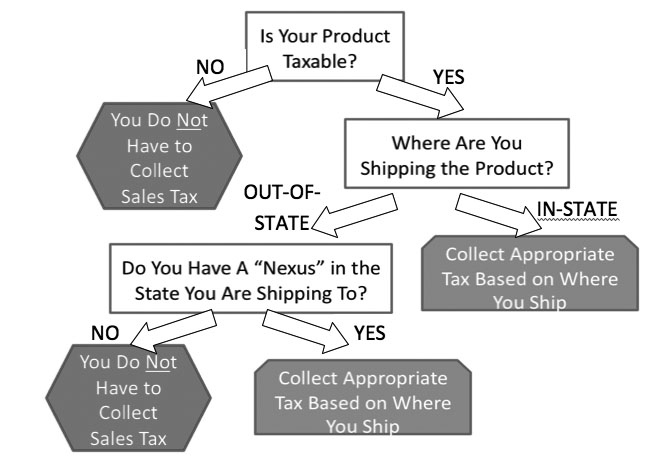

These rulings have given State governments more powers to tax economic activities conducted by Privatized Commercial Firms. As of this year, around sixteen States do not have digital taxation regimes for taxing economic activities conducted in the Digital Realm. The ones that do have such regimes either tax the Seller (with a Sales Tax) or else the Buyer (with a Use Tax). As long as one of the two pays the tax, there is no need to tax the other.

In a world where the concept of Digital Economy is becoming increasingly prevalent and where eCommerce is continuing to challenge the hegemony of the Retail Industry, the question that must be asked from a Federalist standpoint is whether the ITFA should be repealed and replaced in favor of a new law more applicable to the Work-Standard. I am certain that the current law is going to be changed regardless of whether America adopts the Work-Standard or not.

Categories: Economic History

Leave a comment