Consider the following posts to be a discussion of personal finance under Neoliberalism. Here, I will be working with Kapital and Schuld instead of the usual Arbeit and Geld that I have grown more accustomed to over the years. Any of my younger readers, especially those in their teens (be they in secondary school, preparing to pursue undergraduate school or trade school) may benefit from what I have to write on the subject, much of which is derived from personal experiences. The older ones, meanwhile, are probably more interested in how I organize my own day-to-day finances. Whichever the case may be, this is a general rundown on all the important details.

On my own ledger, I track my expenses by categorizing them based on their Reference and Relevance to a specific Personal Property. In Liberal Capitalism, the concept of “Productive/Personal Property-as-Power” does not exist, its absence filled by the more ideologically appropriate Private/Common Property-as-Wealth. The literal absence of Productive and Personal Properties should be the first and foremost consideration because the largest source of Kapital and Schuld in one’s personal finance are whatever Private Properties that they have. With that in mind, my ledger has to be retrofitted for Private/Common Property-as-Wealth.

The two most significant types of Private Properties in America and the broader Western world are the Household and the Automobile. We begin with the Household since there can be specific contexts where somebody might opt for public transportation instead of their own Automobile.

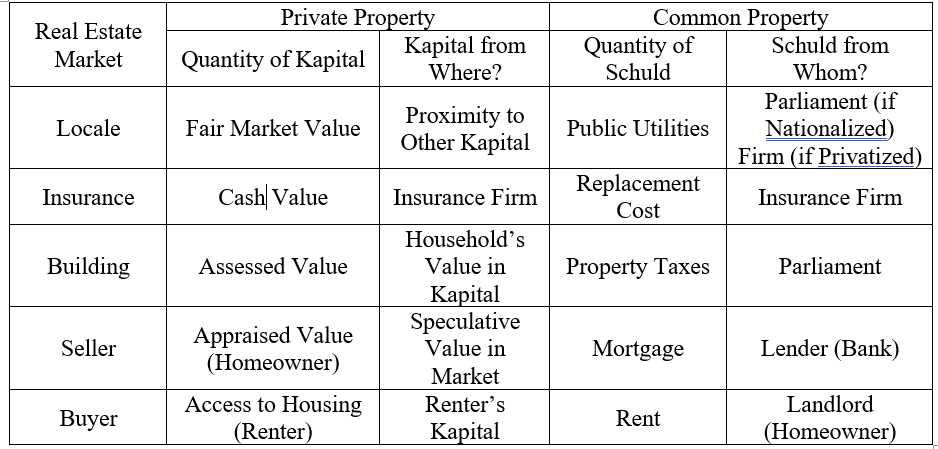

The Household’s Quantity of Kapital originates from the physical location, spatial amenities, and speculative value. They correspond to the Fair Market Value, the Assessed Value, and Appraised Value respectively.

- The Fair Market Value refers to its actual Price on a real estate market in relation to whatever is being developed around the premises. Residential buildings, privatized commercial businesses, important landmarks, and other structures can boost the Household’s Quantity of Kapital due to its immediate proximity to them.

- The Assessed Value denotes the Quantity of Kapital in relation to Property Taxes. Note that the Property Tax is proportionate to the value of the Household in Kapital.

- And the Appraised Value comes from whether the Household is capable of being approved for a Mortgage. Privatized commercial banks finance the economic activities of real estate markets and that in turn makes them responsible for the lending of Kapital to prospective homebuyers as Mortgages.

All three share the same trait: the facilitation of Private Property and its ability to generate a given Quantity of Kapital. Naturally, the solvency–that is, the financial stability–of the Household rests on whether it can keep its Quantity of Schuld down so as to avoid Bankruptcy and thus Eviction. The Quantity of Schuld are the Rents/Mortgages, Property Taxes, Public Utilities–what are deemed “Basic Essentials” in Pure Socialism. And for those in the US, there is also the additional cost from Homeowner Association (HOA) Fees.

- Most people who chose to acquire a Household under Liberal Capitalism did not purchase it at full Price with their own Kapital. Often, they had to borrow a Mortgage from a privatized commercial bank to finance the costs of buying the Household, on the condition that they will pay back the Mortgage with Interest. The concept of Rent comes into play for those who decide to rent a Household, be it an actual house or a small apartment. To rent a Household is to participate in the generation of Kapital through the mere voluntary act of living on its premises, the Schuld created monthly by living there. If the Rent is not going toward paying a Mortgage, it will become payments for Property Taxes and Public Utilities.

- The Property Tax is incurred on those who own Private Property. The Incentive of incurring Schuld through such a taxation measure is to help the Parliament finance the costs of Common Properties. Most Property Taxes are priced according to a Private Property’s Assessed Value, which is, again, proportionate to the value of the Household in Kapital.

- As for Public Utilities, these are of course those Common Properties whose Quantity of Kapital comes from its provision through a middleman. These include water, electricity, natural gas, telecommunications, cable television, and Internet access.

- The lynchpin keeping everything together is of course the Insurance placed on the Household. Just as how the Household is not going to be purchased entirely in Kapital, the same applies if the Household happens to be damaged or outright destroyed in the event of the unforeseeable. The Quantity of Kapital is the value of the Household, the Quantity of Schuld being how much it will cost for an insurance firm to offset the damages.

We can summarize these characteristics into a simple table, split between Private Property and Common Property. Simply put, this is the real estate market’s buyer, the seller, the building, the insurance, and its surrounding locale.

The procurement of the other Private Property, the Automobile, follows a very similar behavioral pattern in the automotive market as the Household was in the real estate market. Just like the Household, the Automobile is not going to be purchased with someone’s Kapital. The purchase would have to be facilitated by yet another loan from a privatized commercial bank, which in this context is an Auto Loan.

There is a Auto Loan made to purchase the vehicle from a seller, who in turn was able to maintain the vehicle from a manufacturer and borrower Kapital from a lending bank. The Automobile itself may have a Warranty as well as possible Property Taxes due to its ability in creating Kapital for the motorist. Alternatively, the Property Tax may manifest itself in other costs, such as having to pay tolls on certain highways and roads. And aside from the insurance, there is also the qualifications that come with being a motorist, such as looking after the Automobile and paying for the necessary licensing and registration.

The rest of one’s personal finances are distinguished between the mundane and those which are tied to Liberal Capitalist ideology. Foodstuffs and lifestyle costs, clothing and laundry supplies, toiletries and cleaning supplies are those mundane costs.

The ones that need to be given special attention are related to healthcare, insurance, loans, savings and retirement. Aside from the two aforementioned cases, insurance also becomes relevant in circumstances where one cannot afford important expenses such as healthcare. Life, Health, and Disability Insurance are all examples. Any Kapital borrowed from loans is a Schuld that has to be paid back with Interest. Whatever Kapital that one has left, assuming they are not going toward the most mundane of expenses, are for savings and retirements. Since humanity is living longer, it has become a sort of Unintended Consequence that there is enough Kapital left for retirements and savings.

I am sure there are other costs, especially those which come with raising a family, but this has been the basis by which I gauge my own expenses and earnings of Kapital and Schuld. Overall, there should be eight areas where Kapital and Schuld are relevant to living under Liberal Capitalism.

- Housing

- Transportation

- Everyday Expenses

- Insurance

- Healthcare

- Loans

- Savings

- Retirement

If one can juggle all eight, one should also be able to realize that some of those categories can and will disappear under the Work-Standard. The characteristics of Arbeit and Geld operate under an entirely different set of parameters than Kapital and Schuld, opening the door to other methods and ways to conduct personal finance. Someday, I will elaborate further in another post.

Categories: Financial Warfare

Leave a comment